Understanding the Mortgage Application Process

What is a Mortgage Application and Why It Matters

A mortgage application is the first official step in buying a home, where you provide detailed financial information to a lender. It matters because it determines how much you can borrow, your interest rate, and ultimately whether you can secure the home of your dreams. This process can seem daunting, but understanding it can save you time and money.

A mortgage is a tool that can help you build wealth, but without proper understanding and management, it can also become a financial burden.

Think of the mortgage application like a job application; just as employers assess candidates for their suitability, lenders evaluate your financial health. They want to ensure that you're capable of repaying the loan, which means they’ll look at your credit history, income, and debts. A strong application can lead to better loan terms and a smoother home-buying experience.

In short, getting your mortgage application right is crucial. It sets the tone for the entire home-buying process and can significantly impact your financial future. So, let’s dive into the steps involved in this essential procedure.

Gathering Necessary Documents for Your Application

Before you start filling out forms, it's essential to gather all the necessary documents. Common requirements include proof of income, tax returns, bank statements, and details of any existing debts. Having these documents on hand will streamline your application process and help you avoid delays.

Consider this step like preparing for a big exam; the more preparation you do, the easier it will be when the time comes. Organizing your financial documents not only helps you present a clear picture to the lender but also boosts your confidence as you move forward. Remember, the lender needs to see a complete view of your financial situation.

Importance of Mortgage Applications

A mortgage application is crucial as it determines your borrowing capacity, interest rates, and the overall home-buying experience.

Keep in mind that every lender may have slightly different requirements, so it’s wise to check with them ahead of time. This way, you can gather everything you need without scrambling at the last minute, making the application process smoother and more efficient.

Understanding Credit Scores and Their Importance

Your credit score is like a report card for your financial behavior, and it plays a significant role in the mortgage application process. Lenders use credit scores to gauge how reliable you are as a borrower; higher scores generally lead to better loan terms. If your score isn’t where you’d like it to be, don’t worry—there are steps you can take to improve it.

The best time to plant a tree was 20 years ago. The second best time is now.

For instance, paying off debts and ensuring timely bill payments can positively impact your score over time. Think of it as building your financial reputation; the more responsible you are, the better your chances of securing a favorable mortgage. Additionally, checking your credit report for errors can help you address issues before applying.

Understanding your credit score can empower you during the mortgage application process. By being proactive about your credit health, you can enhance your eligibility and potentially save thousands over the life of your loan.

Choosing the Right Lender for Your Needs

Not all lenders are created equal, and choosing the right one can make all the difference in your mortgage experience. Take the time to research various lenders, comparing their rates, fees, and customer reviews. This step is crucial because the right lender will not only offer competitive terms but also provide support throughout the process.

Imagine you’re selecting a restaurant; you wouldn't just pick the first one you find, right? You would likely consider the menu, ambiance, and reviews from friends or online sources. Similarly, when choosing a mortgage lender, consider your individual needs, such as flexibility, communication, and expertise in the type of loan you require.

Gather Required Financial Documents

Collecting necessary documents ahead of time streamlines the mortgage application process and helps prevent delays.

Asking for recommendations from friends, family, or real estate agents can also lead you to trustworthy lenders. Ultimately, the goal is to find a lender who understands your financial situation and can guide you through the complex world of mortgages with ease.

The Loan Estimate: What to Expect

Once you submit your application, the lender will provide a Loan Estimate (LE), a crucial document that outlines the key terms of your mortgage. The LE includes important information such as the loan amount, interest rate, monthly payment, and estimated closing costs. Understanding this document is vital, as it allows you to compare offers from different lenders.

Think of the Loan Estimate as a menu at a restaurant; it lists what you can expect and for how much. Just like you’d check the prices and options before ordering, you need to analyze the LE carefully. Pay attention to the interest rate and any fees, as these can significantly impact your overall investment.

If something seems unclear on your Loan Estimate, don’t hesitate to ask your lender for clarification. A good lender will be happy to walk you through the details, ensuring you understand all aspects before moving forward with your mortgage.

The Underwriting Process Explained

After you accept the Loan Estimate, your application moves into underwriting, where the lender assesses your financial information more thoroughly. This stage is crucial, as underwriters evaluate your creditworthiness and ensure that you meet the lender's guidelines. While it may feel like a waiting game, this step is essential for securing your mortgage.

Think of underwriting as a backstage pass to a concert; it’s where all the behind-the-scenes decisions happen. Underwriters will scrutinize your financial documents, looking for red flags or inconsistencies. They’ll also verify your employment and income, ensuring everything checks out before approving your loan.

Understanding the Loan Estimate

The Loan Estimate outlines key mortgage terms, allowing you to compare offers and make informed decisions.

While the underwriting process can take time, staying in touch with your lender can help alleviate any concerns. Being responsive to any additional requests can also speed things along, allowing you to move closer to homeownership.

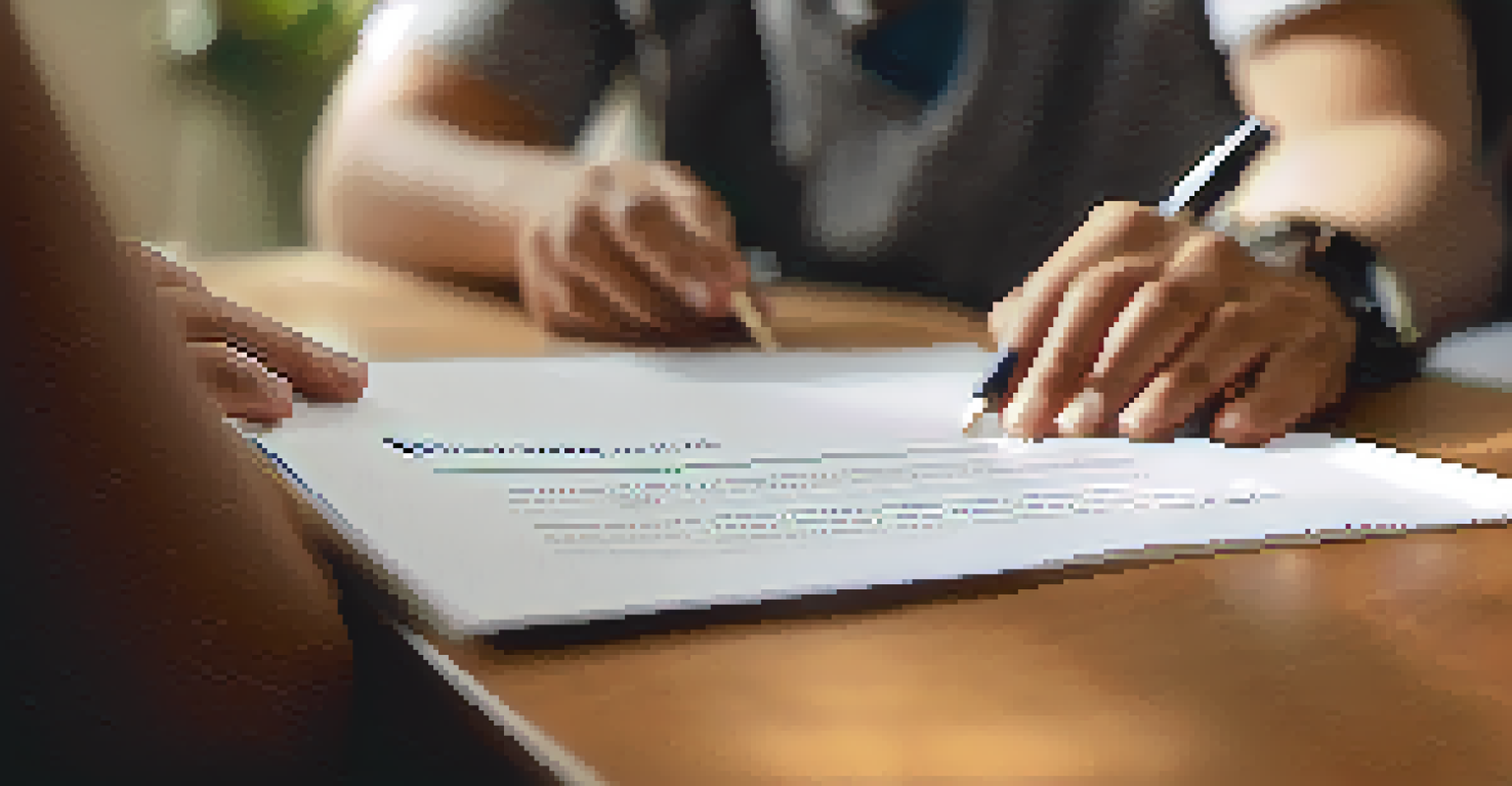

Closing the Deal: What to Expect on Closing Day

After a successful underwriting process, it’s time for closing, where you’ll finalize the mortgage and officially become a homeowner. Closing day typically involves signing a lot of paperwork, so it’s essential to come prepared. You’ll review and sign the closing disclosure, which outlines all final loan terms and costs.

Think of closing as the finish line of a race; it may feel like a long journey, but the excitement is palpable. This is the moment when you get the keys to your new home, making all the previous steps worthwhile. Be sure to ask any questions during this process to ensure you fully understand your obligations moving forward.

Remember to bring necessary items, like your ID and any funds needed for closing costs. Once everything is signed and the lender funds the loan, you’ll officially be a homeowner, ready to start this new chapter of your life!

Post-Closing: Managing Your Mortgage Responsibly

Congratulations! You’ve successfully completed the mortgage application process and closed on your home. However, your journey doesn’t end here; managing your mortgage responsibly is crucial for your financial health. This includes making timely payments and staying informed about your loan terms.

Think of your mortgage like a garden; it requires ongoing care and attention to thrive. Regularly reviewing your budget and making extra payments when possible can help you pay off your mortgage faster and save on interest. Additionally, staying on top of your home’s value can inform future refinancing opportunities.

Lastly, don’t hesitate to reach out to your lender if you encounter financial difficulties. Many lenders offer assistance programs for struggling homeowners, helping you navigate challenges while keeping your home secure. By being proactive, you can ensure your home remains a source of joy and stability for years to come.