Natural Disasters and Home Insurance: What Coverage Covers

What Are Natural Disasters and Their Impact on Homes?

Natural disasters, such as hurricanes, floods, and earthquakes, can strike with little warning, leaving behind a trail of destruction. These events can cause severe damage to homes, leading to costly repairs and displacements. Understanding what constitutes a natural disaster is essential for homeowners, especially in areas prone to such events.

In the midst of chaos, there is also opportunity.

The impact of these disasters can vary widely; some may experience minor damage, while others may face total loss of property. For instance, a flood can ruin not just the structure of a home but also personal belongings, leading to emotional and financial strain. Preparing for these scenarios is not just practical; it's vital for peace of mind.

Insurance coverage plays a crucial role in mitigating the effects of these disasters. Knowing what your policy covers can make a significant difference in your recovery process. This article will guide you through the coverage options available for various natural disasters.

Understanding Home Insurance Basics

Home insurance is designed to protect your dwelling and personal property against unexpected events, including natural disasters. At its core, it typically covers damage to the structure of the home, personal belongings, liability issues, and additional living expenses if you’re temporarily displaced. However, not all policies are created equal, especially when it comes to natural disasters.

There are different types of home insurance policies, such as HO-1, HO-2, and HO-3, each offering varying levels of coverage. For instance, while an HO-3 policy provides broad coverage for most perils, it may still exclude specific natural disasters like floods and earthquakes. Understanding these nuances is key to ensuring you're adequately protected.

Natural Disasters Can Devastate Homes

Natural disasters like hurricanes and floods can lead to severe damage, costly repairs, and emotional distress for homeowners.

Before choosing a policy, it's essential to assess your individual needs and the risks associated with your location. Factors like proximity to bodies of water or fault lines can greatly influence the type of coverage you may require. Being proactive can save you from potential heartache down the road.

Common Natural Disasters and Their Coverage

Different natural disasters require different types of coverage, and homeowners must understand what their policy includes. For instance, standard home insurance policies typically cover fire, wind, and hail damage, but they often exclude floods and earthquakes. This means that if you live in a flood zone, you may need to purchase a separate flood insurance policy to be fully protected.

The best way to predict the future is to create it.

Earthquake coverage is another area where homeowners often find gaps in their insurance. Many standard policies do not cover earthquake damage, which can be substantial. If you live in an earthquake-prone area, seeking additional coverage is a wise decision to ensure you're not left high and dry after a disaster.

It's also important to note that some disasters may have specific deductibles or limits. For example, hurricane damage might come with a separate hurricane deductible that is higher than your standard deductible. Understanding these details can help you prepare for potential out-of-pocket expenses.

The Importance of Additional Living Expenses Coverage

In the unfortunate event that your home becomes uninhabitable due to a natural disaster, additional living expenses (ALE) coverage comes into play. This part of your home insurance policy can cover the costs of temporary housing, meals, and other necessities while your home is being repaired. It's crucial to ensure your policy includes this coverage, as the costs can quickly add up.

Imagine having to stay in a hotel for several weeks while repairs are made after a hurricane—ALE coverage can provide significant financial relief during such stressful times. Without this coverage, homeowners could face a hefty financial burden on top of their existing mortgage and repair costs.

Understanding Insurance Coverage Levels

Home insurance policies vary in coverage, often excluding significant risks like floods and earthquakes, making it crucial to understand your specific needs.

When reviewing your home insurance policy, take the time to understand the limits of your ALE coverage. Some policies may have daily limits or total caps, so knowing these details can help you make informed decisions and avoid surprises during a crisis.

How to Determine Your Coverage Needs

Assessing your coverage needs starts with a thorough evaluation of your home and its contents. Consider the total value of your home and personal belongings, including furniture, electronics, and valuables. This assessment will help you determine if your current policy limits are sufficient or if you need additional coverage.

Next, think about the risks associated with your geographical area. If you live in a region susceptible to specific natural disasters, such as tornadoes or wildfires, you may need specialized coverage. Researching local trends and statistics can provide insight into the likelihood of such events.

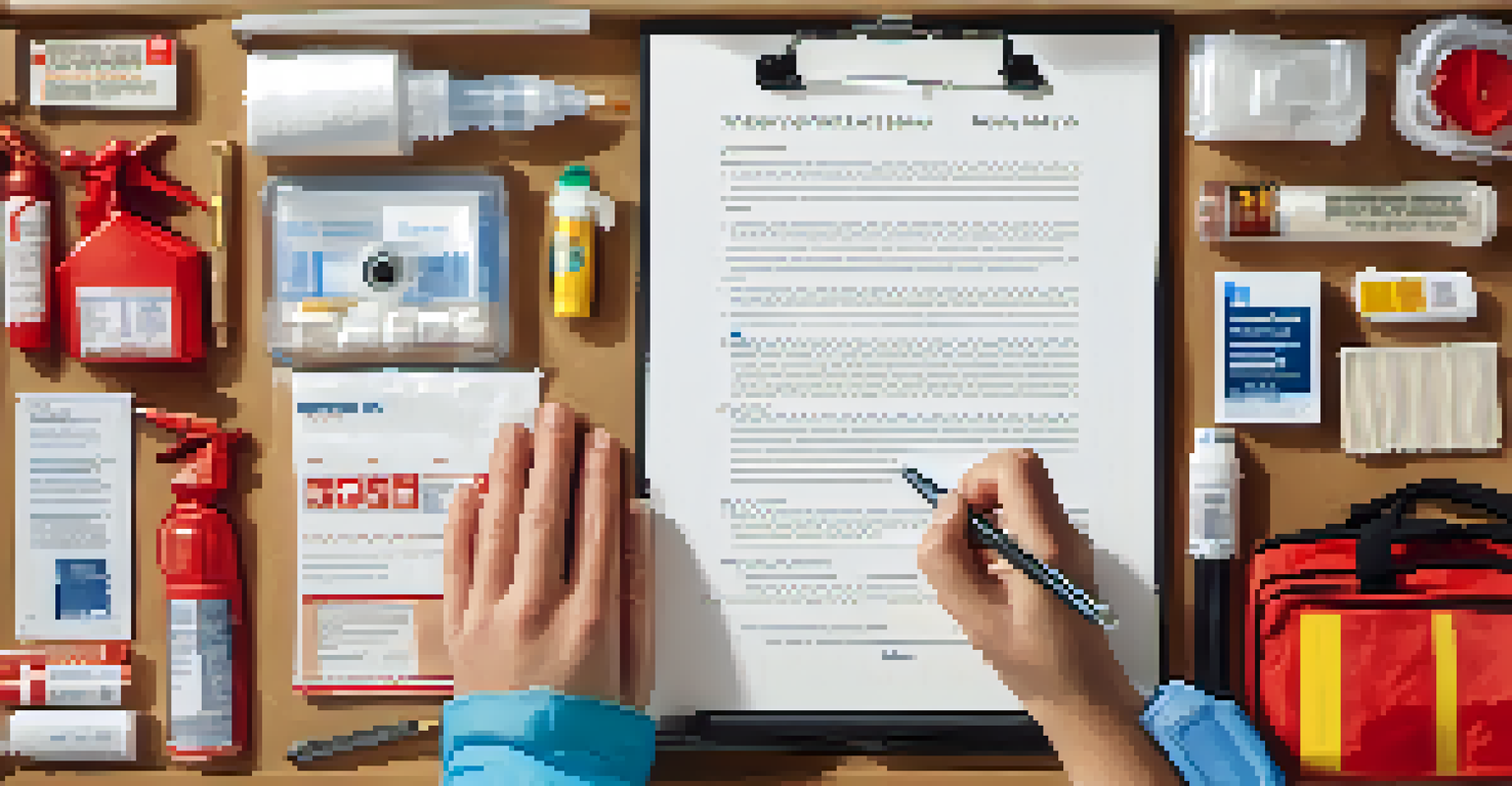

Lastly, it's a good idea to consult with an insurance agent who can help tailor your coverage to your specific needs. They can provide valuable advice on what additional policies may be necessary, ensuring that you're fully protected against the unpredictable.

The Role of Flood Insurance in Home Coverage

Flood insurance is a critical component of home coverage that many homeowners overlook. Standard home insurance policies generally do not cover flood damage, which can lead to significant financial loss during a flood event. If you live in a flood-prone area, obtaining a separate flood insurance policy is not just advisable; it's often necessary.

The National Flood Insurance Program (NFIP) provides coverage options for homeowners, renters, and businesses in participating communities. This program offers both building property coverage and personal property coverage, ensuring that you’re protected from the financial impacts of flooding. Understanding the terms and conditions of your flood insurance can provide crucial peace of mind.

Review Insurance Regularly for Protection

Regularly reviewing and updating your home insurance policy ensures it reflects changes in your home and personal belongings, providing adequate protection against disasters.

Remember, flood damage can occur even in low-risk areas due to heavy rainfall or melting snow. Therefore, it’s wise to assess your risk and consider flood insurance, regardless of your location. Being prepared can make all the difference when disaster strikes.

Reviewing and Updating Your Insurance Policy Regularly

One of the best practices for homeowners is to regularly review and update their insurance policies. Life changes, such as renovations, new possessions, or even changes in family dynamics, can all impact your coverage needs. Scheduling an annual review with your insurance agent can help ensure that you have adequate protection.

Additionally, after experiencing a natural disaster, it's crucial to reassess your policy. Damage estimates and repair costs can fluctuate, and ensuring your coverage reflects the current value of your home and belongings is essential for effective protection. This proactive approach can save you from potential underinsurance.

Don't wait until a disaster strikes to assess your coverage. By taking a proactive approach to reviewing and updating your insurance, you can navigate the complexities of home insurance with confidence, knowing you’re well-prepared for the unexpected.